These days, investors and analysts have to devote plenty of effort in order to get a better understanding of how revenues and earnings of companies develop in the near-, medium- and long-term in the light of the current coronavirus crisis (so do we, see HERE and HERE). But with all the understandable focus on performance, cash generation and the P&L, one should not forget that there are other important value-relevant fundamentals to focus on: pensions for example!

In fact, March 2020 has been a roller-coaster ride for US- and European pension deficits. And this is merely a foretaste to what we can expect during the next months. Be prepared for 2020 being a year of quite a lot of pension madness! In order to highlight the drivers of pension performance in the recent past but also during the coming months we exemplarily shed some light on corporate pension assets and liabilities of German DAX 30 companies. Let’s start with some basic and technical details.

IFRS pension accounting is covered in IAS 19. Corporate pension plans follow one of two possible schemes: a) the defined benefit (DB) scheme in which the employer promises (and is liable for delivering) a specified pension payment, and b) the defined contribution (DC) scheme where a certain amount is paid regularly into an employee’s pension account and then invested by an investment company. While in the latter case (DC), the employer just pays in and the concrete outcome of the investment process is at the employee’s risk, in the former case (DB) the risk is clearly with the employer who made the promise. Because of the employer’s responsibility for the outcome, DB plans give rise to an employer’s accounting liability to the employees. This liability is called the Defined Benefit Obligation (DBO) and it is calculated as the present value of expected future pension payments to employees. For calculation of the present value, the discount rate used is determined by reference to market yields at the end of the reporting period on “high quality corporate bonds”. The duration of these bonds should more or less match the duration of the pension liabilities (IAS 19.83).

As often in practice some parts (or all) of the DBO are covered by dedicated investments (plan assets), the figure on the balance sheet – the pension provision (largely equalling the pension deficit) – is a net amount:

![]()

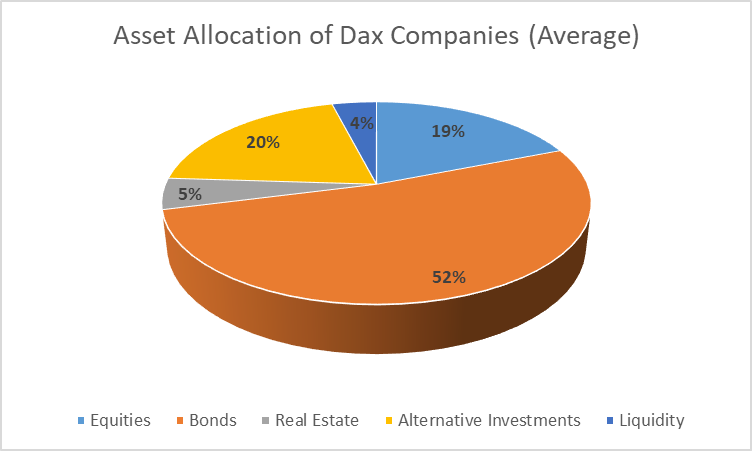

The plan assets – that are usually irrevocably transferred to an external trustee by the company by way of a so called Contractual Trust Agreement (CTA) – in most cases represent a broad portfolio of different investment classes. From the annual reports we know that the German Dax 30 companies showed in 2019 on average the following asset allocation for their plan assets (with quite big differences for single companies’ allocation, e.g. Deutsche Telekom with roughly 70% equities while Munich Re at less than 5% equities).

During February and March 2020 the value of plan assets of DAX companies has massively decreased due to the coronavirus capital market turmoil. DAX companies can still be quite happy that they have such a low equity ratio as compared to e.g. the US-companies which prevented the portfolio of plan assets from even stronger deteriorations.

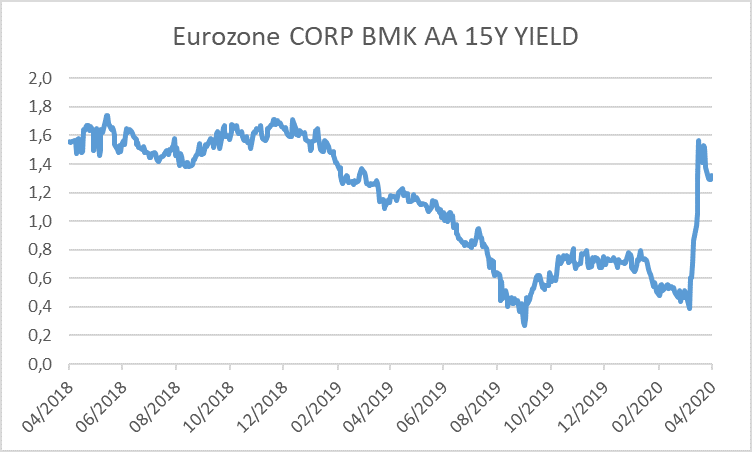

But not only plan assets, also the DBOs of German DAX companies have seen strong value shifts in recent days. The benchmark “high quality corporate bond” yields are usually derived in practice based on an adjusted AA-rated corporate bond portfolio. The average duration is somewhere near 15 years. Below we have mapped the development of 15 year maturity AA-rated Eurozone corporate bond yields over the last two years. Important: The yields shown in the graph underestimate the relevant discount rates for IFRS accounting purposes a bit on average as a 15 year duration translates into more than a 15 year time to maturity. However, the relative development is quite representative for the development of IFRS pension liability discount rates of German Dax 30 companies.

In the graph you can see the strong decrease of the yields since beginning of 2019, mainly driven by a further reduction of the credit spreads. Then, in mid-march 2020, we could see a strong coronavirus-induced jump-up in the yields of roughly 90 basis points from the lows of 9 March 2020. This increase was triggered by a spike in risk aversion together with a sudden decrease of liquidity in international bond markets (something not dissimilar to what we have also seen during the financial crisis 2008/09).

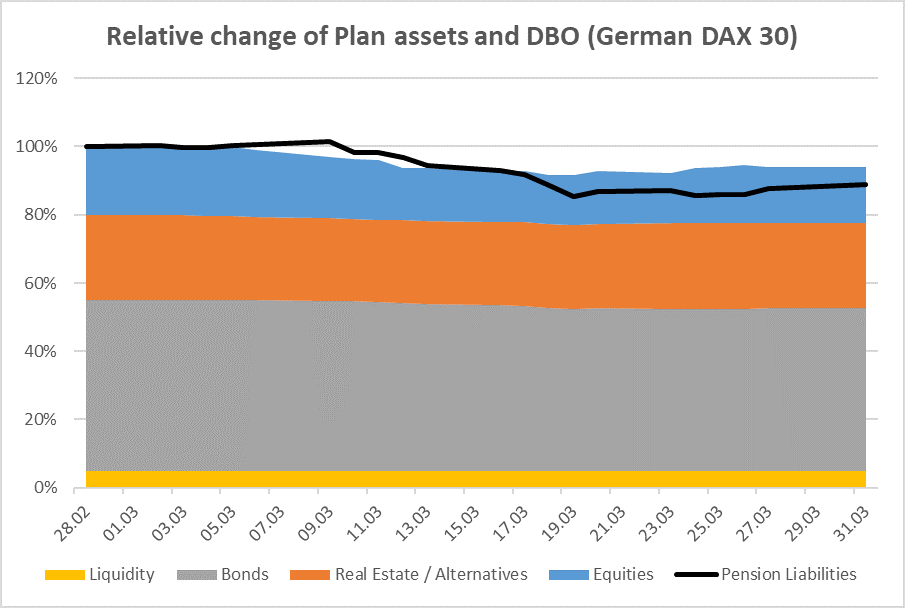

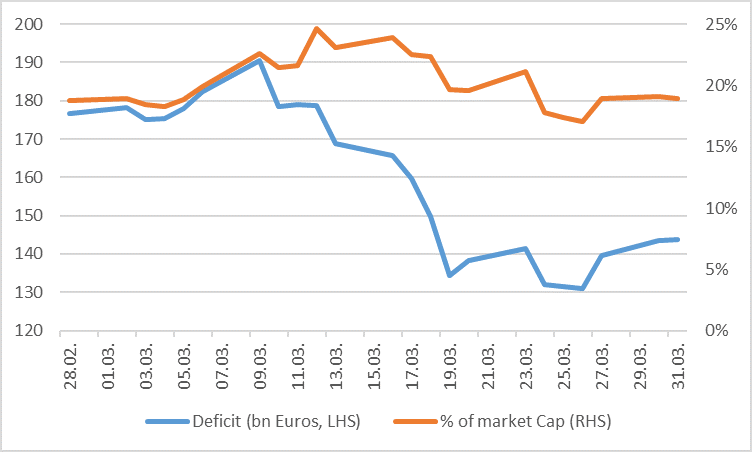

The massive asset value changes (impact on the fair value of plan assets) combined with the sudden and strong jump in discounting-relevant bond yields (impact on the fair value of the BDO) has shaken up the pension positioning of companies quite a lot over the recent weeks. Below we show the relative development of pension assets and pension liabilities of German DAX companies, only during March 2020 (29 February 2020 = 100%). Important: Theses are results of own simulations based on certain assumptions (in particular on portfolio allocation). So the real results might differ slightly from the depicted results.

Due to the big amounts of assets and liabilities the changes do not look super-material in the above chart. However, this changes if we look closer at the numbers.

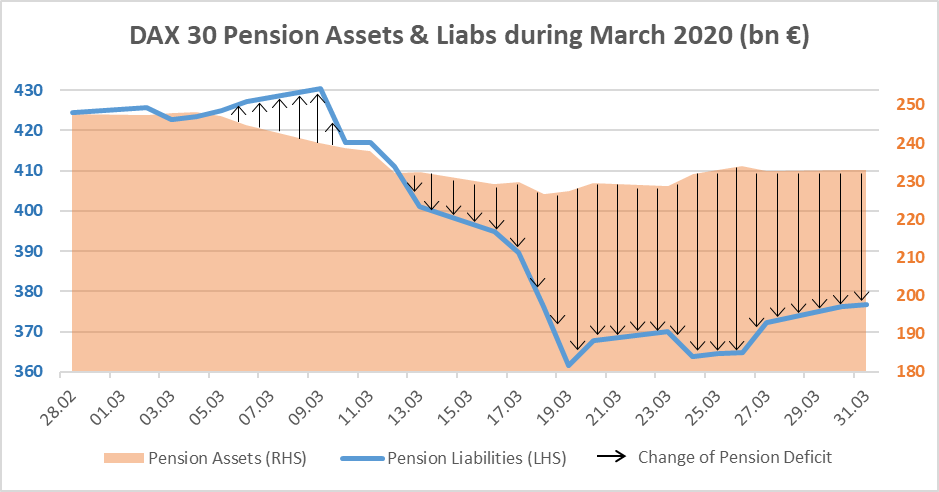

In this graph we can see the big swings in the pension deficits of DAX 30 companies during March. With a starting value of roughly 175 bn Euros (for all companies) the deficit first increased further due to the plan asset value decrease. Starting at 9 March, the benchmark bond yields increased, leading to a lower present value of the pension liabilities which overcompensated the further plan asset value loss and led to a net reduction of the deficit at end of march down to roughly 145 bn Euros – a decrease of almost 20% during one month! And with big swings!

Interestingly, if we look at the total deficit compared to the market capitalization of DAX 30 companies, we can see that basically…. Nothing has changed! The reduction in the deficit is perfectly matched by the reduction in equity market values of DAX 30 companies. At beginning and end of march the combined pension deficit stood at roughly 19% of combined market cap.

But the swings in pension deficits of March 2020 are certainly not the end of the road. In contrast, we can expect to see much more deficit volatility during the year triggered by a) further high uncertainty and nervousness at capital markets across all asset classes and b) further expected high volatility of bond yields with the recently announced 750 bn Euros Pandemic Emergency Purchase Programme (PEPP) of the European Central Bank (which also includes corporate bond purchases) as well as individual fiscal government aids tearing down the bond yields again on the one hand side, while ongoing economic tensions pushing them further up on the other hand side! So be prepared for a hot summer and fasten your seat belt for the next months of pension madness! And this madness will certainly lead to an interesting ride for the DAX 30 companies that already have a high pension-deficit-to-market cap relation, such as in particular Deutsche Lufthansa AG, E.On SE or Deutsche Post AG (Thyssenkrupp AG, the company with the biggest relative pension deficit, is no longer part of our analysis as they were excluded from the DAX 30 last year). In contrast, well-funded companies such as Deutsche Bank AG or SAP SE will not be so much at the mercy of the coming pension deficit swings.

But with all this accounting volatility triggered by pension effects, one aspect will remain more stable in IFRS Profit & Loss statements than in US-GAAP statements. Since the change in IAS 19 pension accounting rules in 2014 companies have to report a „net interest cost“ in the P&L which is calculated by applying the pension liability discount rate to the pension deficit. Before (and still the case in US-GAAP) companies had to apply a dedicated „expected“ return on plan assets which was/is regularly higher than the discount rate and which might be much more prone for bigger reductions in the current environment. But let’s see whether US-companies really change this rate…