The new Coronavirus (Covid-19) is roiling the stock markets. The virus changes the fundamental outlook for many business models and simultaneously brings a lot of uncertainty about the concrete extent of this change. In this blog post we do not want to provide our own market view on Covid-19 nor do we want to make any single stock investment recommendations. We rather want to present an analytical framework listing the main points to look at when performing fundamental company analyses in the light of Covid-19. Of course, this framework is far from perfect and contains a lot of subjective views. And – also as a matter of course – we certainly miss a lot about the concrete development or outlook of Covid-19 as we are no medical experts.

In this framework we only look at the fundamental analytical side with regard to single companies. We do not look at market parameters of valuation functions. A nice post regarding the general stock market picture and the basic valuation effects in the light of Covid-19 has been written by Aswath Damodaran recently (text plus video HERE ). In his post readers will also find some further thoughts on fundamental analytical questions.

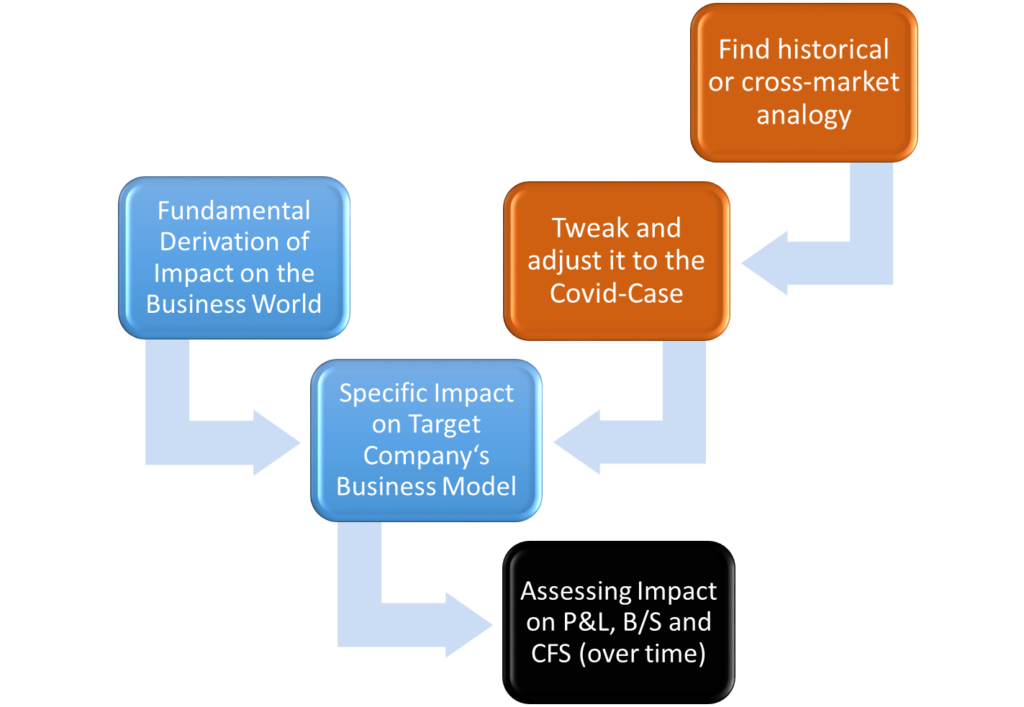

The Basic Approach

We recommend to follow a two-track analysis approach here. This is a standard analysis method in particular (but not only) when dealing with high-uncertainty situations. The first track is a derivative one which uses similar situations or related markets (further up or down the value chain) as a learning tool. This is an important source of information as it is usually very difficult for an external analyst or investor to make sound projections or derive proper reaction effects in a high-uncertainty environment without the experience of what has happened or currently happens in comparable situations. For the Covid-19 analysis it seems to us that the best comparable is the experience with the SARS virus in 2002/2003 – at least as a starting point. The SARS experience is certainly a good general comparable but it is not a perfect mirror of what happens currently in the context of Covid-19. This is why the SARS analogy has to be tweaked and adjusted in a further step with regard to some aspects to make it an even better learning tool for the Covid-19 case.

The second track is the well-known purely fundamental bottom-up approach. Based on observations of what the current effects of Covid-19 are on the broader economy in the respective regions the concrete impacts on the company under analysis (the target-company) are derived. This analysis uses the typical tools such as value chain analysis, Porter 5-forces or PESTEL. In order to make best use of the SARS-analogy as a learning tool it is highly important to regularly benchmark the findings from the fundamental bottom-up approach with the adjusted SARS-analogy. This is an interactive process that takes place several times during the whole fundamental analysis.

The Analogy

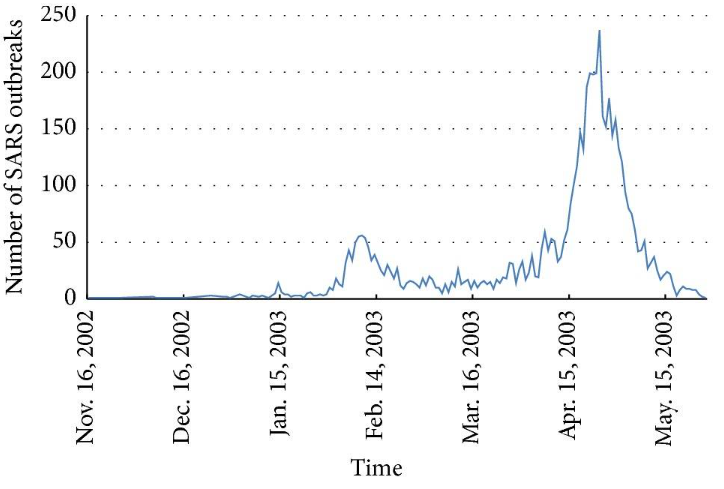

Clearly the best starting point to learn about what implications the Coronavirus has on the business world is the SARS virus from 2002/2003 (the more recent MERS virus was not infectious enough in order to serve as a comparable, and real global viruses such as the 1918 influenza are a bit too heavy as a comparable from today’s perspective and also took place in a totally different business environment). SARS had its outbreak in China in the middle of November 2002 and lasted an overall time of roughly 9 months. In terms of number of new cases SARS followed a typical virus development for connected regions which is not too different from the shape of a bell-shaped distribution picture (or better: a combination of two such distributions). The following graph shows the development of daily new cases of SARS in China.

Source: Cao et al. (2016), Analysis of Spatiotemporal Characteristics of Pandemic SARS Spread in Mainland China, in: BioMed Research International

In the above graph one can see two peaks, both following more or less a bell-shaped distribution. The first one (mid of February 2003) is the peak of the original region Guangzhou and the second one (end of April 2003) is the peak in Beijing after the spreading of the virus.

According to the Cao-Paper, in terms of contagion of not closely connected regions it took about 60 days on average to spread from an affected area to adjacent ones, whereas within-region infectiousness was much higher in densely populated regions than in rural regions (something we can also see above in the chart). Overall, SARS diffused from China to more than 25 countries and summed up to roughly 8,000 cases in total with more than 5,000 in China and another roughly 2,000 in Hong Kong.

Adjusting the Analogy

Covid-19 is in general very similar to SARS from a disease characteristics point of view (this also becomes clear by its alternative name SARS-CoV-2). However, while SARS still stayed quite local – with a focus on China and only two more or less bell-shaped incremental case patterns, see the graph above – we do not know whether this is also the case for Covid-19. Recent news rather indicate a much more global contagion picture of Covid-19 (in line with the seemingly higher infectiousness of Covid-19 as compared to SARS, a bit softened by the lower mortality rates of Covid-19, see Xu et al. (2020), Systematic Comparison of Two Animal-to-Human Transmitted Human Coronaviruses: SARS-CoV-2 and SARS-CoV for a comparison of the two viruses).

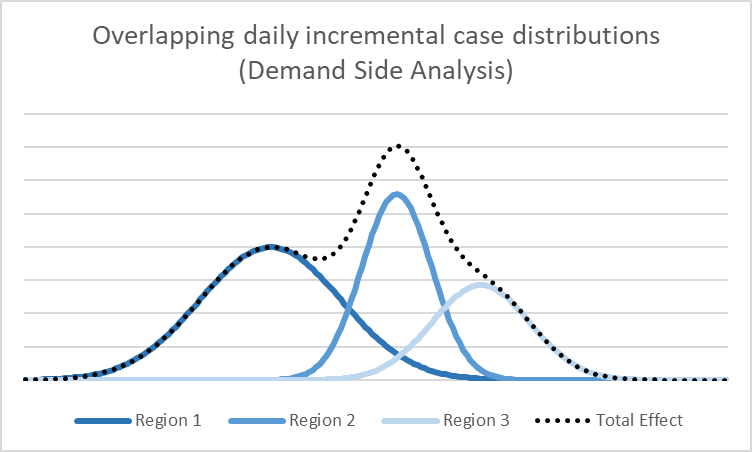

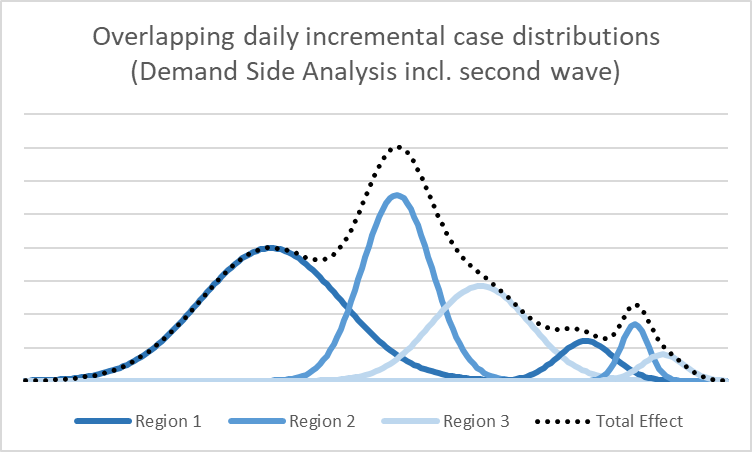

This more global circumstance might make it necessary to follow a multi-regional outbreak projection. I.e. while in the case of SARS it was possible to map the local Asian demand weakness and the production (and hence for many companies: the supply-chain) interruptions with basically one single curve (or two at max), there might be – depending on the exposure of the target company – the necessity to work with multiple time shifted, sometimes overlapping curves, and separately for the cost and the revenue positions of the company. While acknowledging that one can easily over-model this – in particular against the background of the high uncertainty here – we recommend to focus on big regions in a first step with a continuous update as new information comes out. Below we provide an example of a (here unnamed) company in terms of new-outbreak cases. But take care, this still has to be translated into ongoing total cases and finally revenue effects.

Over and above the concrete spreading of the virus, it is also important to note that the economic environment has greatly changed since SARS. In particular, the relevance of China to the world economy has massively increased over the last years. This is the case for the participation and weight in the supply chain for many sectors (today about 75% of technology hardware and almost 50% of components have their roots in China) but also for the revenue side for many business models. E.g. while most European luxury goods companies didn’t have any meaningful revenue exposure at all to Asia in 2002/2003 they now generate sometimes up to 40% of their sales in China.

And finally, duration becomes a critical issue. While SARS was a nine-months effect in total we do not know today how long and severe the Covid-19 effect will last. We come back to this important aspect below.

Consequently it is necessary to go one step back when mapping the fundamental impact of Covid-19 and split the virus development patterns from the economic implications. This doesn’t mean that one cannot learn from the SARS impact but it is highly necessary to adjust it to the new business environment.

Such learning from the past plus tweaking this experience in a second step is a delicate analytical task. An investor always runs risk to stick too closely to the SARS patterns or to deviate too much from it. However, the rule is to here to dare – if in doubt – to make adjustments to the SARS experience if these adjustments follow a clear analytical process. From behavioural economics we know that investors are (wrongly) rather reluctant to make adjustments once they have found a good comparable scenario. This effect is known as the “availability bias” which is the cognitive failure that describes that humans often think that example cases which come readily to mind (SARS) are more representative to the situation under investigation (Covid-19) than it is actually true.

The hard Economic Consequences

In a static observation of what Covid-19 (similar to SARS) brings to the economic environment we can mainly see three effects:

- Production interruptions in the affected regions triggered by work place closures. Due to the heavily interconnected and more and more restrictively timed global supply chain flows this might also have domino effects on many other production steps in regions which are not (yet) directly affected by Covid-19.

- Demand changes which might materialise in a general reduction of demand for certain products/services (and to a higher demand of other products/services) but which might also lead to a shift of consumption channels.

- Less physical exchange and movement in general (in China total passenger travel is roughly 80% below 2019 numbers currently), which might have an impact on sectors which live from physical exchange (e.g. tourism, logistics) but which might also have an impact on the way of exchanging goods and services, i.e. a higher pronunciation of digitally-based flows where possible.

So obviously, the effects are both on the revenue-side as well as on the cost-side. But of course not to the same extent for each and every company. It is necessary to go through output (revenues) and input (supply-chains) markets separately for the target company to get a better understanding of exposure.

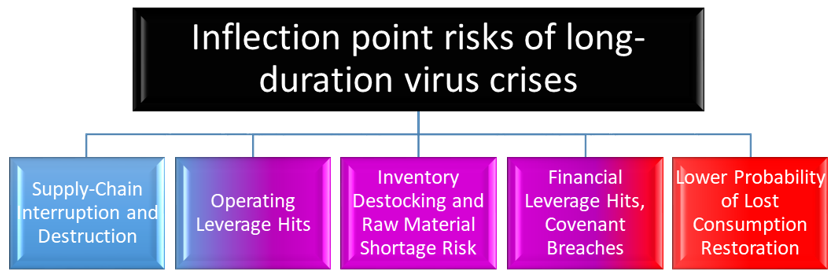

The Question of Duration of Impact

Legend: Blue: Cost-side effects, Purple: Cost- and Revenue-side effects, Red: Revenue-side effects

We have already mentioned the duration problem above. In terms of supply-chain issues it is worth to understand that supply chains can still work (perhaps on a limited basis) if the duration of the problem is not too high. All suppliers sit on certain inventory levels (e.g. Chinese tech producers are on average running a 4 weeks inventory level, as far as we know). These times can be prolonged by reduced production levels and by exhausting some oversupply in certain sectors. In the case of SARS the relatively quick indication of the nearing end of the epidemic (at least since mid of May 2003 it became more and more clear that the worst is over) didn’t destroy too many of the supply-chains at all (although the negative impact was also clearly visible and full restoration took quite some time). But the longer the duration of the impact of Covid-19 the more fragile the supply chains get. Such supply chain interruptions do not only lead to shortages and stops, but also often to quality issues (new unexperienced entrants step in) or higher costs of sourced products for end-producers (with further negative consequences for the final price and hence the attractiveness of supply of final products).

The longer the duration of supply chain interruptions the more difficult it is and the longer it takes usually to restore it. From experience with longer supply chain interruptions we know that restoration is also sometimes a problem of lost trust (as suppliers often go the dirty way in order to deliver or stay in the game in general during the problematic period). The fact that our today’s world supply chains are so restrictive in many sectors and that our production world is so closely interconnected doesn’t make this problem any softer.

Don’t underestimate the supply-chain issue for your target-company. It might not seem obvious that the supply-chain has some contact to the already affected regions. But for many businesses supply-chains are quite complex and it takes more than a first glance to spot the critical parts of the chain.

On the revenue side, the longer the impact takes the bigger the risk that some of the lost product or service sales during the crisis will not be recovered afterwards. Short crises often only lead to a pure delay of consumption or general buying activity, but the longer a crisis takes the higher the probability that the lost sales will not be recovered – simply because customers have found other ways to deal with it. In general, the rule is that for durable goods the probability of only being delayed is much higher than for certain services or consumption goods which are usually much harder to be made up after a crisis. But even automobile company Daimler doesn’t expect a pure delay of its China operations. In a recent statement, the company announced that it expects to lose roughly 30,000 car sales only in Q1/2020 and hopes to recover only half of this throughout the rest of the year 2020.

Furthermore, some business models rather show seasonal revenue generation patterns. This could be in yearly terms (e.g. Christmas business for some retail companies) or in quarterly terms (e.g. end of quarter cumulation of revenue generation for some capital goods companies). As we are now still a bit away from the end of the first quarter of 2020, it is worth to take these uneven-sales-effects properly into account in a revenue projection.

In terms of inventory levels of target companies, it is worth to have a closer look at the structure of inventory before making a judgement on how they will be impacted by a longer duration crisis. In a world where pressure on business models comes from both sides (revenues and supply) companies are generally better positioned if they have a larger share of raw materials – as they can use the time for ongoing production work and are not that much affected by supply shortages. In contrast, a larger share of finished products is rather negative in these times as a longer-term crisis might force companies to get rid of these products at lower prices or alternatively have to suffer from a longer-term capital tie-up.

Also on both the cost and revenue side, an additional problem of duration becomes relevant. Companies that run a high fixed cost base (i.e. high operating leverage) can sustain a certain shock for some time but not necessarily for a very long time. Operating leverage aggravates the effect of top-line shocks on the income level which might challenge the mid- to long-term suffering ability of high operating leverage companies with regard to fixed cost coverage. The filing for insolvency of Japanese cruise operator “Luminous Cruise” last weekend is a typical example of the dangers of high operating leverage in such a virus crisis. But operating leverage is also a big topic currently to (still functioning) Chinese suppliers. Their margins are usually quite thin, meaning that their ability to sustain a longer crisis is not super high.

Similar is true for companies that show a quite tense financial leverage. All the discussion about the optimum capital structure (buzzword: Tax Shield) might now turn to the negative for companies that for optimisation reasons run their businesses like a ride on the debt-razor-blade. This is perhaps not a very general problem of the economy but it might hit single businesses quite heavily. We will certainly see more discussions about covenant breaches and similar in the coming months (outcome unclear). For the same reasons the question of how much cash companies have on the balance sheet might become a very important issue in the coming months. In short: An analysis of single business models in the context of Covid-19 should always bring along an analysis of financial flexibility, too!

Summary: Duration impact is not at all a linear path. There are certain inflection points to every business model where things suddenly turn to the bad. These points have not been tested extensively in the SARS phase, so don’t think that this is not possible in the Covid-19 phase. If for certain business models the inflection point is hit, then there is a big chance that they do not follow the V-shaped recovery that most companies showed in the SARS-phase but rather a U-shaped or even an L-shaped recovery in some cases. But to analyse this is a highly company-individual issue.

In terms of non-linear effects of long-duration virus crises it is also worth noting that for some business models which approach a problematic operational situation due to the Covid-19 effects the topic of indirect insolvency risks might become relevant, i.e. the fact that in times of corporate crisis some stakeholders (customers, employees, suppliers, etc.) might react adversely and try to lose the connection to the company – which usually reinforces the crisis. However, we do not want to go deeper into this point here.

What about the Long-Run?

Letting aside the question what “long-run” really means as we do not know exactly how long the acute phase really takes (but probably longer than the SARS phase) we also have to deal with the time after the virus has disappeared or at least normalised. So, while Covid-19 has and will have an impact on the global economy during the acute phase, with all the experiences of similar (although not perfectly comparable) viruses the impact should be a temporary one in general. This does not mean that single businesses will be punished even sustainably but at least in an overall context it seems as if there will be no long-term destruction to doing business. But to be honest, we do not know exactly today.

What might be a long-run effect of Covid-19 is that certain business structures will be readjusted by some companies. In the face of a fresh understanding of the fragility of supply chains we wouldn’t be surprised if some companies will go away a bit from the very thinly calculated supply chain structures in order to better secure business continuity – which might come at the cost of higher input prices. But also at the benefit of lower risk to the normal going concern plan. We heard some comments from some companies in this direction but we should wait whether the actions suit the words.

Another potential long-run effect is that digital solutions gain in general relevance where possible. E.g. in the retail business at least part of the physical store raison d’être is still that for many customers it takes longer to step away from long-established habits (a fact that we can also observe by the different shopping patterns of generation Y and Z customers on the one hand side and older customers on the other hand side). This metamorphosis process might be sped-up in the face of Covid-19 with some customers getting inevitably more accustomed with online retail now.

Another sector that might be sustainably hit from the forced, accelerated consumption patterns change is the education sector. In China, education companies already offer more and more online-courses since the Covid-19 outbreak.

Finally, a lot of the long-run prospects in general will depend on whether the virus crisis also leads to capital expenditure (CapEx) cuts which in turn will reduce capacity in the affected sectors also in the long-run – with all the good and bad consequences for different business models.

But these are only some ideas or thoughts, not much of a thorough analysis behind it. We only want to highlight here where a change to a new-normal is possible in the long-run but it might well be that Covid-19 does not change the business world materially once it is gone (or reduced to a normal level).

Where to look at to stay up-to-date during the ongoing virus crisis?

At our opinion the best way of staying up-to-date is via the Webpages of the World Health Organization (WHO) on situation reports (HERE) and on events (HERE).

In general terms we think it is also worth to regularly adjust the new-infections scenarios for both the demand regions as well as the supply regions of the target-company. E.g. we currently see a little risk that once the quarantine period is over in China and with a relaxation of mobility control the number of new transmissions will increase again. This might become also a topic for other regions during the virus period. And this might lead to a second wave of new cases.

Some (off-piste) Sector and Business-Model Thoughts

Below is just a short wrap-up of where to look at for certain business models from our analytical experience. We do not want to comment on the obvious ones such as Airlines, Tourism, Gastronomy, Autos, Freight, Luxury Goods, etc. or companies which have a strong China exposure in general as you can read a lot about them in the press or can make you own analyses. We provide only some sideline-thoughts on some not so obvious sectors and business models.

First of all, Covid-19 is not bad for every company. In particular to business models that can circumvent the reduced physical-exchange problem such as certain online-service-providers (mobile time spent by customers has increased massively in China during the last weeks in businesses such as online-gaming, news, education and also healthcare [Alibaba Health!]). Furthermore, there are business models that provide some sort of solution to the Covid-19 situation such as in chemicals (some latex-glove and disinfectants producers) or some medtech companies. And there will also be some beneficiaries in the pharma industry one day.

For life insurance companies, Covid-19 could become a problem if the virus spreads global to a larger extent. The asset-liability management of life insurance companies is usually based on a very high predictability of policy-outflows. If the average life expectancy in the contracts would be shocked asymmetrically, this might negatively impact the whole financing construct of these companies. SARS, however, was too mild to meaningfully negatively impact life insurance companies.

In contrast, as far as we know, the underwriting risks for most European reinsurance companies are rather modest, despite a strong increase in exposure to Asia since SARS. Most of today’s policy risks are related to death benefits. For property & casual, in contrast, the impact of virus-related business interruptions is more or less excluded from most policies today (a consequence of the SARS experience).

For capital goods companies there is no clear direction of development. It all depends on the concrete end-markets. Some of them are highly negatively affected (e.g. those with exposure to autos, shipping, etc.) and some even benefit (e.g. those with focus on healthcare topics).

For some consumer staples companies such as alcoholic beverage producers it is worth highlighting that in China roughly 50% of beer consumption takes place out of home. This means that the current drop in restaurant and bar visits in China might have a meaningful impact on some international consumer staples companies.

For commodity-based business models such as utilities, mining or steel companies all depends on what the impact of Covid-19 is on commodity prices. For coal-dependent business models – at least as it seems as for now – the impact is rather negative. China is a big net-consumer of coal and the coal consumption is very low currently (it has not recovered after the Lunar New Year break). For steel things are not that clear. China is the biggest producer but also the biggest consumer of steel products. Once things normalise, it will also be interesting how market prices react to the time lags (restoration of the Chinese production chain will take some time due to ramp-up phases and some necessary maintenance work; additionally there is a time lag until the deliveries of products will arrive in markets like the EU (some weeks)). And finally, if the crisis takes longer, there might also be some consequences on CapEx decisions in the commodity sectors. This in turn might lead to long-term effects on the supply-demand-relationship and hence on commodity prices.