IFRS is quite clear on what should be reported in the income statement for determining operating profit measures: Everything that generally qualifies as a revenue or an expense! There are no exceptions. Admittedly, this has not always been the case but it is the strict rule since the early 2000s. US-GAAP basically follows the same procedure today, but only since January 2015.

Before, the accounting standards allowed to separately disclose certain effects which might be seen as unusual and infrequent, i.e. extraordinary or exceptional and hence not representative for the future. The idea of the old rule was that this better allows investors and analysts to understand the underlying corporate performance. It is, however, not a big surprise that companies often generously defined what they think is extraordinary or non-underlying. There were several businesses out there which ‘unfortunately’ suffered from extraordinary negative earnings impacts every year. These ‘poor’ accident-prone companies redefined each single year what is “infrequent” or “unusual”, even if exactly these infrequent events have been happening quite frequently and the unusual ones were quite usual business.

It is also nothing new that companies try to report their own view about sustainable performance outside the regular accounting (called “Non-GAAP” measures) which is sometimes sound in terms of presentation of a normalised profit, but often a pure palliation and whitewash of the real performance. Domino’s Pizza’s presentation of its ‘underlying profit before tax’ is certainly one of a kind (see LINK)) but there are many other examples out there.

Today, however, some companies have even found a more creative way of presenting their own view of performance. They include their adjustments directly into the income statement, i.e. in the audited part of annual reports. One might wonder how this is possible against the background of standard setters’ rules – but the answer is quite straightforward: They simply provide two perspectives (their own and the official version) in one single statement – one next to the other. Strictly speaking they do nothing wrong because still they show the IFRS or US-GAAP view explicitly. But what should an investor think of such a presentation? The company’s alternative view is not only audited but also part of one of the holy grails of financial statements: The statement of income itself! With at least a little bit of trust into auditors’ work one usually would have to give some credits to the company’s own presentation of performance, or wouldn’t you? Well, this can be quite misleading in many cases…

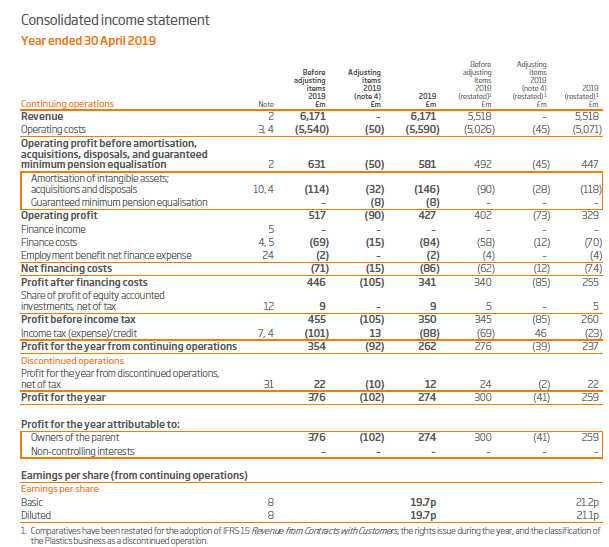

Below we provide the presentation of the consolidated income statement from the annual report of DS Smith plc, a big UK packaging solutions provider (cartons, plastic, etc.). In the left column you can see the corporate view, second to left column the adjustments and in the third column the IFRS numbers.

Source: Eurofins, AR 2018

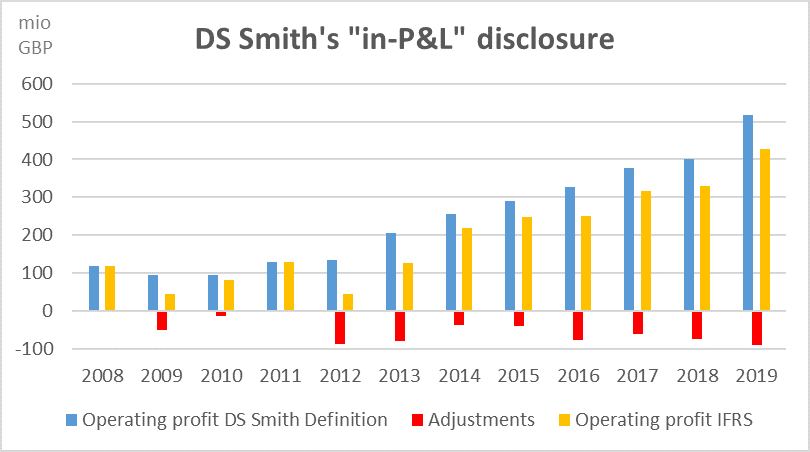

Obviously the “adjustments” for operating profit from the company’s perspective to the IFRS perspective are negative in both of the last two years, a common picture of non-GAAP performance presentation. But two years are not enough to judge on DS Smith’s understanding of performance. In fact, we can go back many years and always see the same picture: At least since 2012 the company records very stable negative adjustments from their view down to the IFRS view. And these operating profit adjustments are highly material. They average at roughly 20% of the company’s operating profit since 2008.

Now one might throw in the argument that the DS Smith view is perhaps more in line with the economic situation of the company than the IFRS view (and of course, sometimes deviations from the hard IFRS rules are really necessary to shed a brighter light on the economics of the company, fundamental analysts know this all too well). But first we would answer that this still should not show up in the audited income statement but rather being a management commentary which should be communicated separately.

And second, this argument does not really hold for DS Smith from an economic point of view. Looking closer at what determines the performance deviations we basically find that it is mainly certain legal fees, integration costs, M&A due diligence costs, etc. In fact, part of DS Smith’s business model is buying other companies each and every year. This is the main driver of its revenue growth. M&A is part of the DNA of DS Smith. Nothing wrong with this, but M&A deals also require due diligences and the integration of the new businesses. These are normal ongoing charges for this business model, nothing to exclude from the performance (and this sort of charges will continue to show up in DS Smith’s FY 2020 again). So DS Smith wants to be judged based on its top-line performance but obviously not by the costs it has to suffer along with this process.

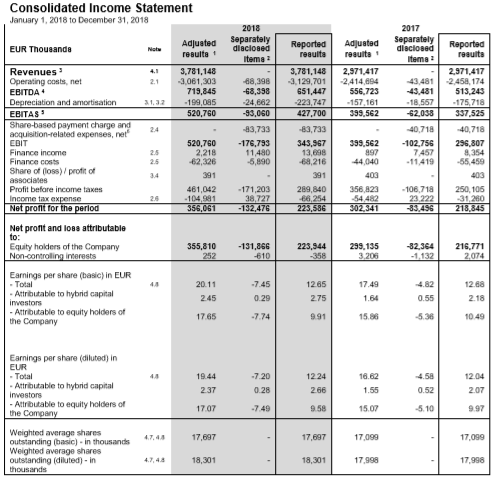

DS Smith is certainly not alone with this performance presentation. There are several other examples which follow the same strange presentation path. One of them is presented below: Eurofins Scientific SE, a Luxembourg based medical laboratories company.

Source: Eurofins, AR 2018

We think it is not necessary to state here that this sort of presentation is really targeting at getting the most out of ‘alleged’ accounting credibility: the blessing of auditors, and the penetration into one of the core statements of financial reporting, the income statement. And this really makes it a very dangerous way of information dissemination.

Certainly, financial analysis is not only about reading and making up your mind on the future economic and financial impact, it is also a lot about trust in what auditors allow to be presented as an audited information which serves as the basis for decision making. This does not mean that financial analysts do not have to do their own analyses to get to a decision basis but it means that analysts need a clear understanding of the degree of accuracy and reliability of the numbers. And what DS Smith, Eurofins and others present is unfortunately far away from what we should expect to get (and usually actually get) as a basis of information from audited financial reports.