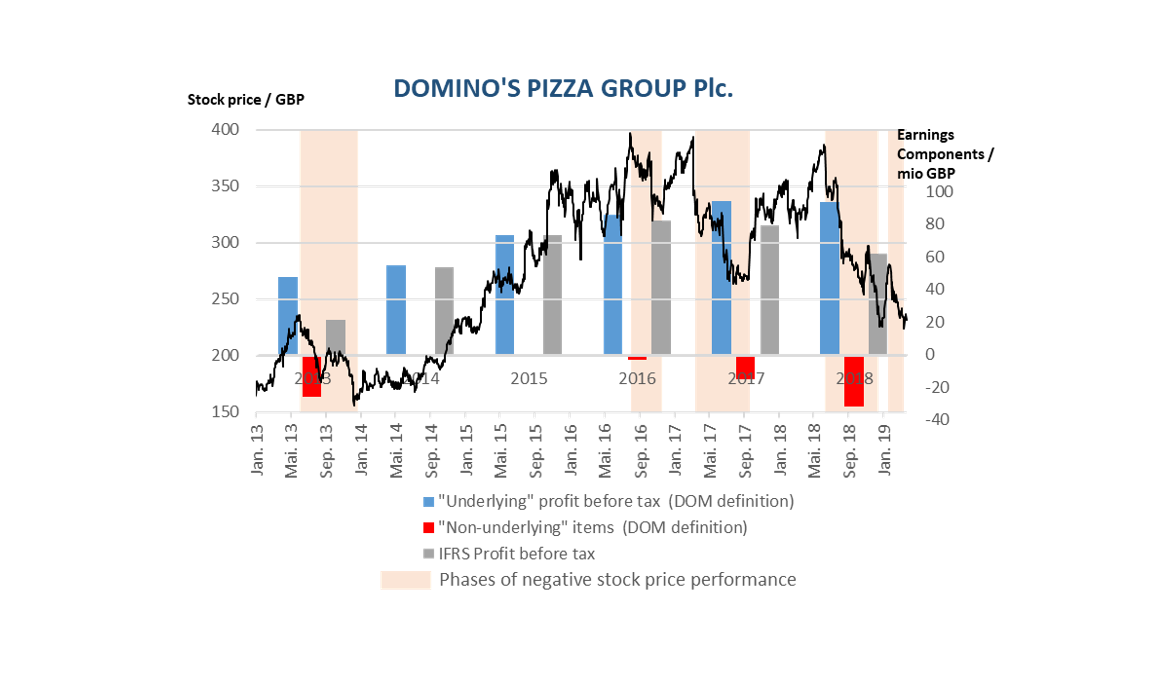

No, business is not developing in a great way for Domino’s Pizza Group Plc (DOM). A weak Scandinavian business, high debt burdens, a lot of tension with franchisees who require a bigger share of earnings, and communication confusion around the intensity of these tensions. But at least the reported numbers look ok. According to the 12 March 2019 preliminary results report, the 2018 “Underlying profit before tax” is at 93.4 mio GBP, basically level with last year’s 52-week performance (2017: 94.4 mio GBP). And despite it is not an IFRS-measure, it is the profit number the company sees as the relevant one when talking to investors.

Below this underlying earnings number line, however, there is another line in the report which is worth some deeper analysis. It is called “Non-Underlying Items before tax”, which are items that are “unusual or infrequent in nature”, according to the company. In 2018 these items amount to minus 31.5 mio GBP, i.e. cutting out a third from the underlying profit and leading to a total (IFRS) profit before tax of 61.9 mio GBP. And based on this total profit DOM is now down 22.2% as compared to last year (although non-underlying items have been negative in 2017, too).

Of course, there is principally nothing wrong with presenting the results with a focus on the underlying figures. For investors it is certainly highly interesting to understand what Domino’s earnings basis is that serves as an indicator for future earnings development. And so it is absolutely correct to strip out unusual or infrequent items… if they are indeed unusual or infrequent!

Unfortunately they are not in the case of Domino’s Pizza – at least not all of them. When looking at the notes of the report we can find e.g. 7.7 mio GBP integration expenses for the Norwegian and German business (which is a super-normal cost of a growing business and will show up again while the company is further growing), 1.9 mio GBP of ramp-up expenses for a new supply chain facility (which was allegedly calculated as a shortfall as compared to “normal” efficiency of the business, meaning there is a 1.9 mio GBP too high performance included in the underlying earnings) and more than 14 mio GBP of impairment charges on international businesses which mainly followed only one or two years after the acquisition date (and which are clearly at least in parts indicating a weaker future performance and are certainly not in-full unusual or infrequent). In short, Domino’s reported “underlying” earnings are not a good indicator of the future and carry several elements that have a recurring character. In our view this earnings number clearly overestimates the real earnings performance of Domino’s Pizza, and it does so quite a lot.

When further analysing the recent past of the reporting of Domino’s Pizza we can see that 2018 was not an exception. In contrast, we can find a couple of years with material “non-underlying items”. However, in none of the years there was an extraordinary positive effect (Why not? Where is e.g. an adjustment for a non-sustainable charging of franchisees?). Even worse, when comparing Domino’s accounting practice to its stock price performance we can see an interesting correlation of recording “non-underlying items” and times of bad performance. Even in terms of severity. Honi soit qui mal y pense.

But Domino’s Pizza is not alone with such a proceeding. Trying to save a bit of performance awareness in the eyes of investors in tough times by refocussing their concentration to more positive “underlying”, “recurring”, “core” or “adjusted” earnings is a quite popular move by companies. Swiss bakery company Aryzta AG published during nearly its whole stock market descent from 18 CHF/share in mid-2014 down to 1,40 CHF/share today an adjusted net profits number that was often much more than double the size of the IFRS-earnings. And Rolls-Royce (currently also in a state for transformation and restructuring) just recently reported underlying earnings for 2018, excluding 1.3 bn Euros of exceptionals. A big part of this is related to fixing charges for the underperforming turbofan engine Trent 1000, clearly highlighting Rolls-Royce’s understanding of underlying earnings being the equivalent of a blue-sky business environment performance.

Sometimes, we can even find whole industries which create their own earnings definition: When AstraZeneca Plc. in late 2012 announced that they are switching to an exclusion of product related amortisation and research & development impairments from its core earnings, they were the last of the big European pharmaceutical companies to apply this definition. By that time some investors have already given up to complain about pharmaceuticals accounting, others even applauded the now better comparison with peers. However, group pressure and comparability or not, there is no reasonable economic explanation for why in AstraZeneca’s (and in the other peers’) changed core earnings definition internal research flows into earnings as expenses while third-party research will never show up there (to name just one of the economic problems with the pharmaceuticals “core” definition).

And finally a funny one: Although not on a company level, Australian Macquarie Group Ltd. once published for its single units a profit split – but excluding the contribution from the bonus pool. Against the background of the materiality of bonus payments as a cost component in an investment bank, this really comes closest to the often told “profit before cost”-joke.

But how to deal with this problem from a valuation and analysis point of view? We think, for investors a couple of aspects are important to keep in mind when reading management’s earnings adjustments:

- IFRS earnings do not always do a good job as an indicator of future earnings. Problematic areas include (but are not limited to) asset recognition vs. expenses, value adjustments vs. cash expenses, one-time revenues, etc. Therefore, when management adjusts them to their own view for information reasons, it is not wrong per se.

- However, the incentive for blue-sky reporting is quite high here. Therefore investors should make sure that they have understood every single item that is subject to adjustment and check it for reasonability.

- Important: If you as an investor really want to extract “underlying” earnings from an IFRS measure, don’t stop at expense-adjustments. Also go for revenue adjustments. For many companies you will find a lot of positive aspects, too, that are unusual or infrequent in nature. As such adjustment is not really done by companies themselves, emphasizes the problem of blue-sky reporting tendencies in the real corporate world.

- Even if you feel a certain item is indeed worth being excluded from the earnings base, first have a look at the recent past of the company’s reporting. Some companies are “accident-prone” and report the same ‘unusal’ item more or less every year, which often makes it highly ‘frequent’ in nature.