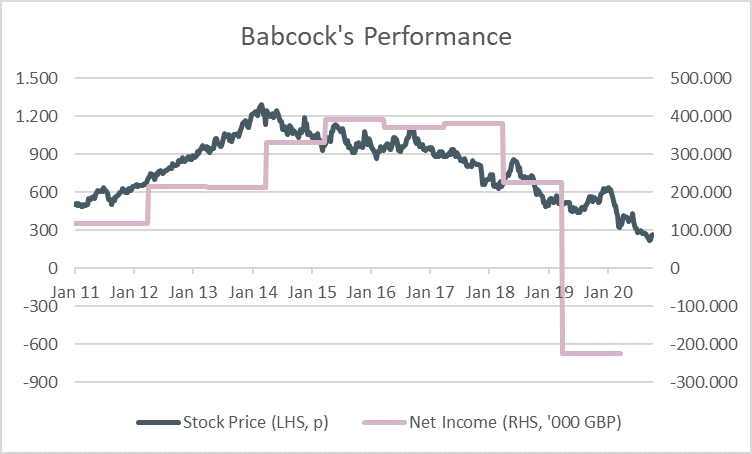

London-based Babcock International Group Plc. is a multinational engineering support services company with a strong exposure to public clients. The company usually manages large multi-year contracts with sometimes complex structures. For some of these contracts Babcock is the sole manager (mainly in fields where there is no or only few competition), many other contracts are run as joint projects together with partners. Core strength and simultaneously core weakness of Babcock’s business model is its longstanding relationship to the UK Ministry of Defence (MoD). While this relationship opens the door for many projects, it is also a huge cluster risk as the MoD is by far the single biggest customer of Babcock. In fact, its weak operating and stock market performance over the last years is to a non-negligible part due to a downturn in government orders.

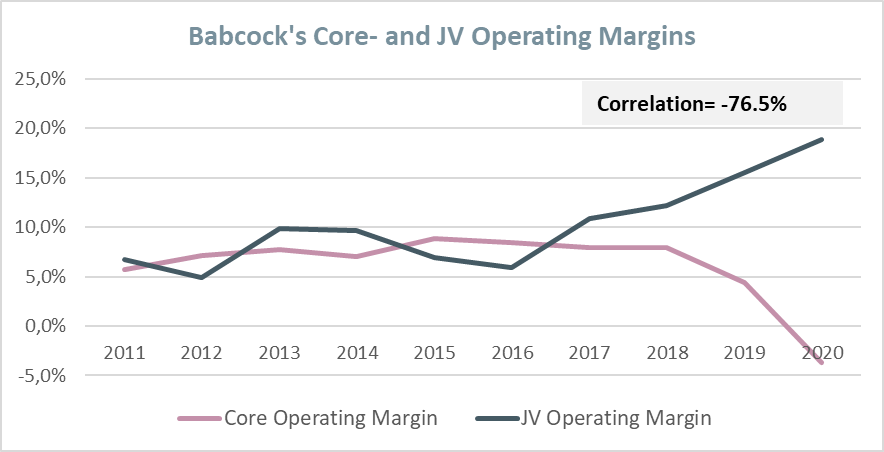

Fundamentally analysing Babcock has never been easy as the multi-year, individualistic and (for outside investors) largely opaque nature of contracts has greatly obscured the true economic picture of the company. Furthermore, Babcock often uses a lot of leeway in its financial reporting which management labels as ‘prudent’ or ‘conservative’ (and which it often is in the beginning years of contracts). This makes forecasting of earnings very complicated and not rarely served for more or less bigger surprises in the past. Finally, it is not clear whether accounting leeway is consistently applied to the whole portfolio of activities as the performance of core business and JV-business has diverged massively during the last years (at very high negative correlations).

We are going to have a closer look at the trickiness of retracing and understanding the accounting proceeding of Babcock by shedding some light on the treatment of one of the bigger JVs of recent years – Holdfast Training Services Ltd. (Holdfast). Holdfast was a JV created in 2008 (initially together with Carillion Plc) to undertake a 30-year contract for the UK MoD to provide training infrastructure and services for the Royal School of Military Engineering. Until the sale of Holdfast in 2020, Babcock owned 74% of interest. However, it could not fully consolidate the business as with regard to the minority shareholder “unanimous decision making is required over key decisions which drive the relevant activities of the business.” (Source: Babcock AR). Hence it had to treat Holdfast as a JV.

The general accounting setting for Holdfast was pretty clear. With the release of IFRS 11 Joint Arrangements (applicable since 2013 resp. 2014[EU]) the former policy choice of proportionate consolidation for jointly controlled entities (Joint Ventures, JVs) has been eliminated. Since then a joint venturer has to account for any interest in a JV by using the equity-method of accounting in accordance with the IAS 28 Investments in Associates and Joint Ventures (which was reissued together with IFRS 11). This means, JVs are to be treated like normal associates from an accounting point of view (the rare exemptions from this rule do not apply in the case of Babcock/Holdfast).

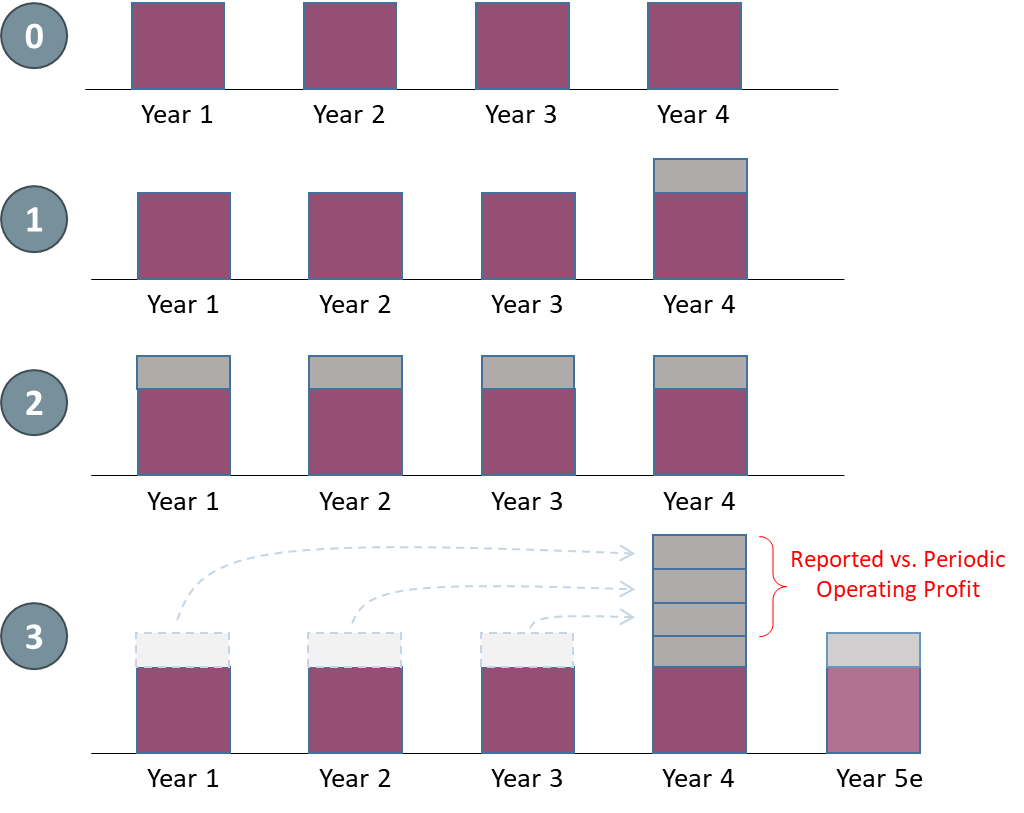

Within this setting, however, Babcock applies some special techniques and reporting variants. The first one is the recognition of resetting effects. The Holdfast project – like many other such projects at Babcock – have certain contractual reviewing points in time. At these points Babcock discusses with the customer the progress, the riskiness and the performance of the project. If there is necessity to adjust the remuneration for the project due to differences of reality with initial expectations, then a three-step process takes place. In the hypothetical example below, the project is remunerated according to the contract terms until in period 4 a review takes place (situation 0 below).

The first step (1) of the adjustment process is the determination of adjustment amounts (based on the comparison of reality and contract benchmarks). The second step (2) is the retrospective application of the adjustments. According to many of the Babcock contracts, adjustments are not only made for the review period (and the future periods) but they are also applied to past periods – retroactively. This should serve as a correction for any misestimates at the beginning of the contract (which is actually not the real reason at Babcock, we will explain this below). However, as the financial reporting for past periods is already done, these adjustment effects for past periods have to be cumulatively reported in the review-period – a catch-up accounting (3). This leads to the strange situation that – in case of a positive adjustment – review period earnings are very high and not at all a good measure for this periods earnings power, nor for future earnings. In the example below, period-5-earnings should go down from Period-4-earnings by three grey blocks to the level of the big purple plus one grey block – all other things being equal.

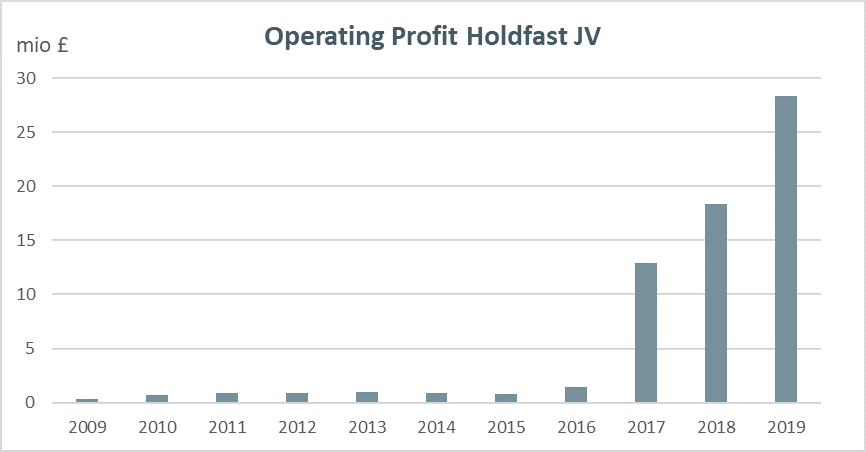

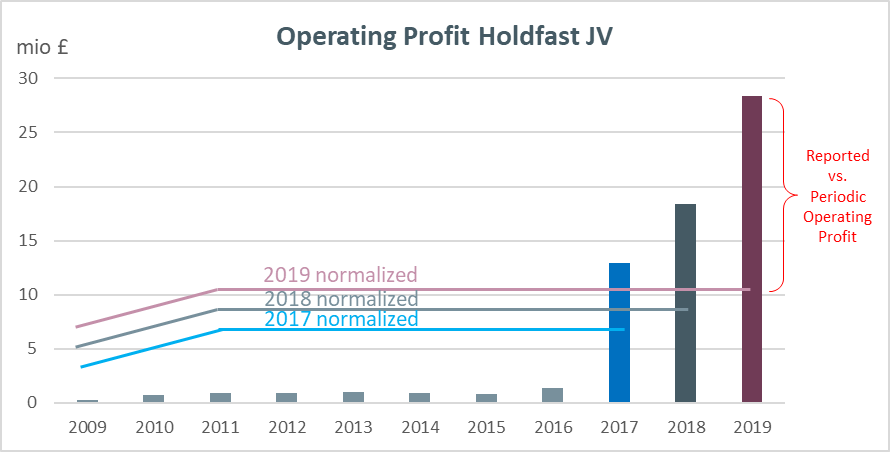

If such adjustments were random – depending on real out- or underperformance of Babcock’s projects – this would be tricky enough. However, in the case of Babcock they are systematic which makes things even more complicated. Let’s have a look at the actual Holdfast performance (here on an operating level).

Obviously, the performance of Holdfast skyrocketed since 2017. This was the time when the 10-year reviewing events started. Here review did not only take place in 2017 but also in 2018 and 2019. The normalised earnings number after all these reviews, i.e. the operating profit expected for 2020, is roughly at 11.5 mio GBP.

Three points are important here:

- These adjustments are not due to a better than expected performance of Holdfast. They follow a systematic path. Babcock intentionally starts out with low earnings in the first years of the contract in order to allow for a step-up and some growth in the latter years. In the Full Year 2018 Earnings Call, CEO Archibald Bethel explained: “So what happens in Holdfast, as a 30-year contract, Babcock’s prudent contracting position, as always, during that first 10 years, we took a very low profit margin as we had so much of the contract still ahead of us.” (Source: Thomson Reuters Streetevents, Full Year 2018 Babcock International Group PLC Earnings Call). Whatever the motivation behind this proceeding is, it is not very helpful for investors. How ‘prudent’ is Babcock? Unclear, a forecast of future adjustments is hardly possible. Does Babcock apply the same level of ‘prudence’ in every project? No, for some more, for some less. This also makes forecast of adjustments or earnings paths nearly impossible. In contrast, a fair assessment of margins and earnings – which could get out- or underperformed, but not in a systematic way – would much better allow for earnings forecasts and also for a sound stewardship assessment (how well does Babcock in its single projects?).

- At least twice investors were taken by surprise here. The first one was the initial adjustment effect in 2017 and the second one was the last adjustment effect in 2019. Regarding the latter, management even guided investors down to a normalisation in 2019 in its annual report 2018: “We expect Holdfast joint venture profits in 2018/19 to step down by £5-10 million” (Source: Babcock AR 2018, p. 45; 2018/19 here means: the financial year ending in March 2019, in our graphs year 2019). This was at a time where Babcock must have known whether there are further reviewing possibilities or not.

- The three year review process with these cumulative effects has some non-immaterial consequences for some fundamental performance measures that are used as a benchmark for management remuneration schemes, see for example the 2016 performance share plan criteria below (see also HERE for an explanation why three years is such a magical number for investors distraction).

Source: Babcock AR 2019, p. 121, own emphasis.

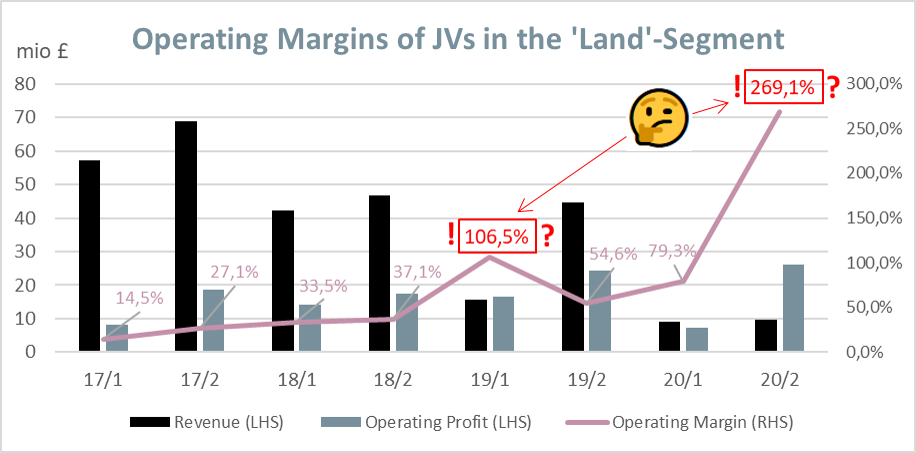

However, this is not yet the end of Babcock’s JV accounting quirks. In its segment reporting Babcock reports performance for its consolidated business and its JV business separately. This makes sense against the background of the high relevance of JVs for this business model. The Holdfast JV falls into the “Land”-Segment of Babcock.

In the ‘Land’-performance presentation, however, Babcock applies a quite strange perspective. For some reasons, it includes the revenues from the Holdfast JV as part of the consolidated business performance, but the operating profit of the Holdfast JV as part of the JV performance. Moreover, Babcock even presents operating margins as one of the three core measures for the segment.

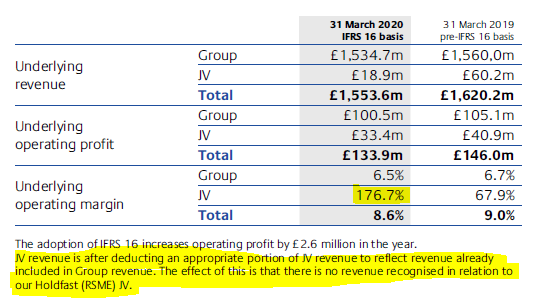

Source: Babcock AR 2020, p. 75, own emphasis.

As a consequence of this split-proceeding, reported margins are totally distorted. In the table shown above, the FY 2020 JV-margin is shown at 176.7% (!). But it will even get more bizarre if we look at the half-year numbers (H2-revenues and -profits are calculated as the difference between full-year numbers and reported H1-numbers).

With the operating margin was already above 100% in H1/2019, it reached an unbelievable 269.1% (!) level in H2/2002. Moreover, the whole JV reporting is super-volatile. Revenues are not rarely fluctuating by more than 100% over time – sometimes even within one reporting period.

Why this way of segment reporting is chosen is a huge enigma to us. Usually such obvious mismatches are somehow related to management remuneration schemes but we could not find any clear sign for this in the annual reports (however, we could also not fully understand all details and criteria of the remuneration scheme from the remuneration report).

Anyway, at times where the operating business shows clear signs of weakness, we think management would help investors a lot if it turns into a more transparent way of accounting for its JVs in particular and its whole contract portfolio in general.

Disclaimer: We hold no economic stake in the company involved in this blog post – in whatsoever direction. We base our analysis on imperfect information and hence we might be wrong with some conclusions. This is just our subjective view and no investment recommendation at all!