Times of crisis always bring out two distinct kinds of bad accounting behavior (along with a lot of good accounting behavior, of course) – one of them is obvious, the other one rather not so. The obvious one is that some companies will try NOT to record all the negative that the crisis requires them to do. The motivation of CFOs of companies which follow this behavior is to a) present the company better than it actually is in these troubled times, and b) not to run into any procyclal problems (where bad circumstances lead to negative reporting results lead to even more negative investor reactions). But the first motivation is bad and the seond one is wrong. Presenting the company better than it is might help management but not adressees of the reporting. And pro-cyclicality of timely accounting is perhaps a problem of financial institutions sometimes but not for non-financial companies – showing economic negatives timely in accounting is explaining reality, not shaping reality. But whatever the motivation of CFOs is in this case, this accounting behavior is most often seen by companies which already feel the water up to their neck and which simply want to keep a last line of defence.

The not so obvious accounting behaviour, in contrast, is more subtle in nature. And it is usually shown by companies that are rather amongst the outperformers during the crisis. This behavior is called ‘Cookie Jar Accounting’. Here companies put some cookies into a jar when they are not hungry (i.e. build up some reserves when they can afford it) only to grab those cookies out of the jar when they want to eat them (i.e. releasing the reserves when they need to). The grandmaster (?!) of cookie jar accounting is still Nortel Networks Corporation, a meanwhile insolvent Canadian telecommunication equipment vendor company. The company structurally built up different pools of reserves in the late 1990s and early 2000s only to relase them later when Nortel needed it, e.g. in the first and second quarter of 2003 where this technique allowed to turn around economic losses into accounting profits or at least to largely erase these losses. The cookie jar strategy of Nortel was to just meet guidances or bonus levels of management, but not exceeding those targets. This allowed to intertemporally flatten performance and optimise management remuneration. Or putting it with the words of Nortel’s head of controlling in an email to his colleagues: “[Nortel’s] general approach is to sand bag good news and close ‘hard’ to the forecast.”. More about this interesting case can be found in the SEC-documents, e.g. HERE (where also the former quote can be found).

The coronavirus-crisis is a great time for cookie jarrers because usually the big hurdle for them to build reserves, e.g. via provisioning or impairments of depreciable assets (i.e. laying a lower basis for future depreciations), is that they need a strong economic argument. Why should well performing companies show negative accounting effects?, auditors ask for good reasons during normal times. But during this current crisis even well-performing companies find arguments to record some negatives – it is all hidden in the big macroeconomic picture.

In order to get a bit of a taste about the accounting behavior of companies in the first coronavirus-reporting, i.e. in Q1/2020, we screened the S&P 500 for any coronavirus-related impairments, provisioning or extraordinary expenses. We clustered the companies into 10 deciles according to their stock market performance between 20 February 2020 and 31 March 2020, with the first decile being the best performers and the 10th decile being the worst performers. The idea behind this clustering is that the best performers could be seen – in economic term – as the companies being the least negatively (or even positively) affected by coronavirus, and the worst performers being the ones that are most heavily affected by this crisis. We use data from Thomson Datastream and we focussed on US companies here because of better data availabilty.

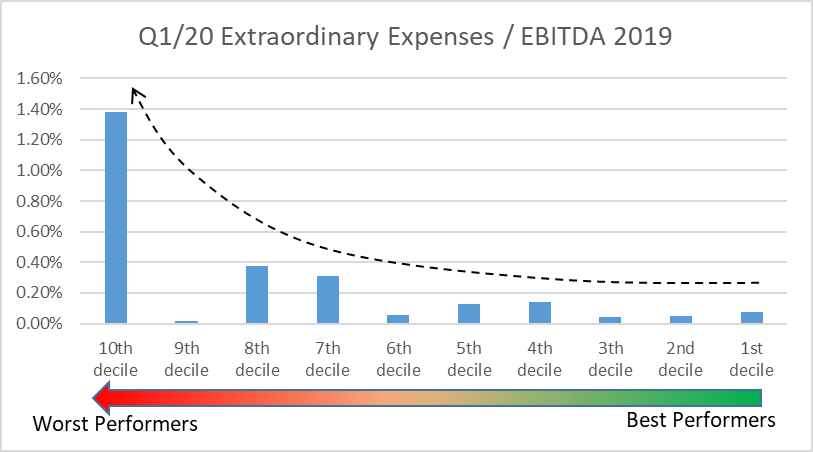

We first have a look at Q1/2020 extraordinary expenses due to coronavirus (scaled by EBITDA 2019). Here are the results.

This picture is well inline with what one should expect in a normal accounting world. The worst performers show the highest relative extraordinary expenses and the amounts decrease with improving performance. It is worth mentioning that it is not helpful for cookie jar accounting if one records some losses via extraordinary expenses as these do not provide a basis for future reversal. Consequently, we mostly see quite reasonable accounting treatments of the well-performing companies. E.g. Netflix, which in Q1/2020 nearly doubled its expected number of new subscribers and performed in the 1st decile of our analysis, recorded expenses “due to paused productions and the establishment of a hardship fund to provide relief payments to workers impacted by the pandemic.” (Source: 10Q). This makes sense in our eyes. However, what is a bit surprising in this graph is the low level of extaordinary expenses in the 9th decile.

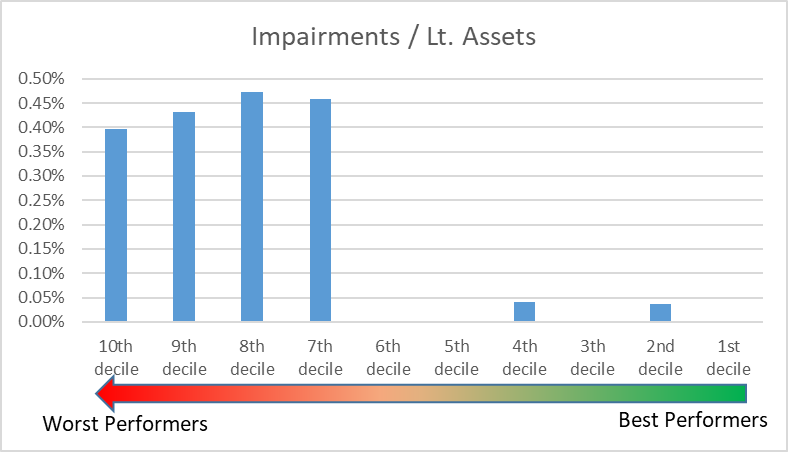

The next graph shows the coronavirus-related impairments (scaled by goodwill and intangibles 2019).

It is worth noting here that usually the degree of management leeway is higher for recording (or not recording) impairments than for recording (or not recording) extraordinary expenses. As a consequence, we can see here the first indications of 10th-decile underrecording. While still the lowest performing 4 deciles make up almost all of the impairments, the 10th decile is showing the lowest relative level amongst these four. The impairment in the 2nd decile comes from Kla Corp., a process control system supplier to the semiconductor industry, and relates to two acquisitions that have been recently performed (i.e. where the fair value of the goodwill has certainly been close to the accounting value of the goodwill) and does not indicate any irregularities in our eyes.

The third graph relates to Q1/2020 one-time provisions in relation with coronavirus (again scaled by EBITDA 2019), and it is quite an interesting one.

Building provisions still offers a higher degree of accounting leeway than extraordinary expenses or impairments. And hence, if companies absolutely do not want to record provisions they might here more easily find ways to abstain from recording than for other expenses or even impairments. This is also what we can see in the graph. In particular the worst performer companies (i.e. the 10th decile) show a surprisingly low level of coronavirus-provisions. This really is an indication of loss accounting reluctance once companies are already massively under the gun from an economic point of view. On the other side we do not see much of provision recording of outperformer companies, i.e. not a lot of indication for cookie jar accounting.

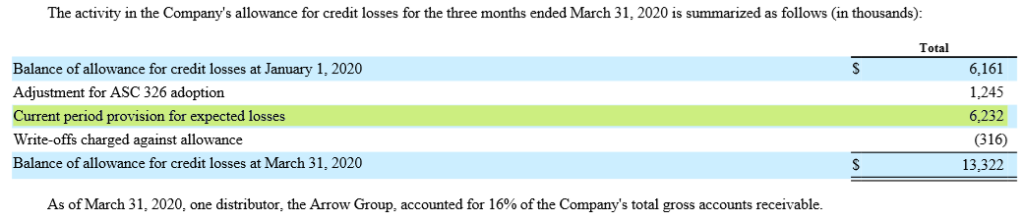

But even if there is not much provisioning in the low deciles we can still read an interesting aspect from the graph. In the first decile we find Citrix Systems, Inc., a software company that provides SaaS and cloud services and which is a clear beneficiary of the coronavirus crisis. Its business is really booming and still the management was able to record a provision. But what are you provisioning for if everything goes better than planned? Exactly! For the decreasing creditor quality! Admittedly, it might not look unreasonable to go this way in the current environment. And we do not know exacly about the creditor structure of the Citrix clients. However, with the expierence of the financial crisis 2008/09 we know that this is a common way of general-crisis-beneficiaries to put cookies in the jar which can later be taken out again. But lets see how the creditor quality of Citrix in the coming quarters develops.

Source: Citrix Form 10Q, Q1/2020, p. 13

Summary

In this blog post we show the results of our S&P 500 Q1-reporting screening. We found some indications of corporate loss accounting reluctance but only mild indications for systematic cookie jarring. However, we also have to admit that today cookie jarring usually takes place in a more subtle way than in earlier years and hence an in-depth analysis of single companies would be necessary to find out more. But this is beyond the scope of this blog post.

Disclaimer: As always, we hold no economic stake in the company involved in this blog post – in whatsoever direction. We base our analysis on imperfect information and hence we might be wrong with some conclusions. This is just our subjective view and no investment recommendation at all.