Unilever has just announced a couple of days ago that they have changed the way of how to tackle hyperinflationary accounting topics for the calculation of one of its core KPIs, the “organic sales growth” (see HERE). From now on Unilever will include Argentinian and Venezuelan inflation capped at 2% per month in this measure. The 2%/monthly limit is based on the idea that this is an inflation growth which is JUST at the limit of what IFRS sees as a hurdle rate for the transition to “hyperinflationary” accounting in a compound perspective over three years. Before, Unilever did not include any price growth from Argentina and Venezuela in its organic sales growth measure since the time the countries have been treated as “hyperinflationary”. Result of this new procedure: From now on organic sales growth rates look better than before: ca. 30 bps for H1/2019 and we estimate a similar 6-months-impact in the near future.

Admittedly, Argentina is a tricky one for many companies. The Argentinian economy has been suffering a lot over the past years. Skyrocketing inflation rates of 40%-50%, an ongoing depreciation of the Peso (with capital controls now in place) and weak consumer demand. This is not only a complicated environment for doing business but also for the financial reporting of companies. Unfortunately, there is no absolutely clear standard of treatment of hyperinflationary environments which makes comparisons among companies quite difficult in many cases. In this article we want to have a closer look at the different sources of comparability problems in the context of the accounting hyperinflation treatment: a) the general problem of what qualifies as a “hyperinflationary country” from an economic point of view, b) the specific problem of the different qualifications as a “hyperinflationary country” in US-GAAP vs. IFRS, c) the differences in the concrete accounting application in US-GAAP vs. IFRS once a country is seen as “hyperinflationary”, and c) the room for manoeuvring for companies when they disclose their core non-GAAP KPIs.

Quick-and Dirty: Basics Hyperinflation Accounting (IAS 29 and ASC 830)

In a hyperinflationary environment the nominal value of assets and liabilities changes very quickly in local currencies. Additionally, in most cases the local currency shows an ongoing depreciation as compared to the currencies in the stable currency regions such as the Euro zone or the USA.

The idea of hyperinflation accounting in both IFRS and US-GAAP is now to better account for these characteristics by allowing for a more current cost oriented measurement of assets, liabilities and corporate performance in the respective country operations. This is mainly done by:

- Restatement of local balance sheets for the effects of change in buying power caused by inflation

- Indexation of local profit & loss statements to account for inflation effects during the period

- Inclusion of inflation-driven value changes in monetary assets and liabilities in the local profit & loss statements

- Translation of the (indexed) local profit & loss statement at the year-end exchange rate instead of the average exchange rate

Economic qualification as a “hyperinflationary country”

While in principal the idea of hyperinflation accounting is sound, it is also clear from the explanations above that it can make quite a quantitative difference whether it is applied or not. In particular for really high inflation rates the transition from normal to hyperinflationary accounting is not smooth at all. For lower inflation rates, in contrast, the number-jumps from before to after the application of hyperinflation are much smaller. Hence, investors’ general wish for balance sheet consistency calls for rather choosing a low bar for qualification as a hyperinflationary country here.

However, hyperinflation does not really sound like ‘lower inflation rates’. While there is no clear sound economic definition for what is hyperinflationary, or better for where does normal inflation end and where does hyperinflation start, typically the limits in all available subjective man-made definitions are much higher than those which would allow for a smooth transition. Not a big surprise but not good for accounting consistency.

US-GAAP vs. IFRS: specific qualification as a “hyperinflationary country”

The standards setters (both IFRS and US-GAAP) add further to this problem. First, they see very high inflation rates as a starting point for hyperinflationary accounting – even if compared to other available measures. The reason for this proceeding is that the concrete application of hyperinflationary accounting is quite complex. Additionally, hyperinflation accounting is a break to our traditional historical cost basis. And so, standard setters rather want to make the hyperinflation case a big exception. This is perfectly understandable and makes absolute sense from my (and many other market participants’) perspective in terms of real world accounting application. But again it adds further to the problem of non-smooth transition and lack of balance sheet consistency.

Making things even more complicated, standard setters are quite divided about the concrete set of criteria for accounting qualification as a hyperinflationary country. E.g. IFRS requires 5 specific indicators – (1) population shies away from local investments, (2) a relatively stable foreign currency is the preferred numéraire, (3) inflation is actively taken into account in prices for sales on credit, (4) interest rates/wages/prices are linked to a price index, and (5) the cumulative inflation rate over three years is approaching 100%. US-GAAP, in contrast, follows a two-step approach – (1) check whether the cumulative inflation rate exceeds 100% for the last three years preceding the start of the specific reporting period. If this is the case the country is hyperinflationary. And (2): if this is not the case, then further economic judgement and analysis is to be applied in order to come to a conclusion.

Obviously the two approaches are different, though they share some similarities. It is also worth mentioning that simply relating to the common indicator on cumulative inflation growth of 100% over 3 years is not always helpful as in many of the high-inflation countries there are simply no reliable inflation indexes available.

The existing differences between IFRS and US-GAAP had concrete consequences in the recent past. E.g., Argentina was seen as fulfilling the criteria for hyperinflation for periods beginning after June 2018 according to US-GAAP. For IFRS, however, it took longer until Argentina was seen as hyperinflationary (due to some more strict requirements on uniformity and comparability between companies). But once IFRS have seen the criteria fullfilled the accounting treatment was applied retrospectively, i.e. starting January 2018. It goes without saying that such differences in application are also not really helpful for comparison of accounting statements between IFRS and US-GAAP.

US-GAAP vs. IFRS: Application

Not only are there timing and qualification differences between US-GAAP and IFRS, there are also differences in the concrete application of hyperinflation accounting in practice. Without going into all the details, but the main difference is that in US-GAAP there is not a direct translation from adjusted financial statements to the home currency of the mother company but rather the foreign entity’s functional currency is changed into a non-hyperinflation-country currency. In most – though not all – cases this is the USD. This different proceeding in application further decreases the comparability between US-GAAP and IFRS.

Core non-GAAP measures – here: organic sales growth

Financial accounting rules are one thing, performance presentation another thing. And whenever there is room for economic interpretation then there is also incentive for companies to present themselves a bit more attractively than they really are. This is particularly true when we talk about important non-GAAP KPIs which are not hard-bound by accounting standards. To get a better understanding of how this is the case here we below have a look at disclosed “organic sales growth” rates of international consumer staples companies which traditionally always had some activities in the Argentinian or Venezuelan market. And consumer staples companies are generally a good example case for looking isolatedly at sales growth measures as they usually do not have material costs in the respective foreign currency.

- Economic Perspective

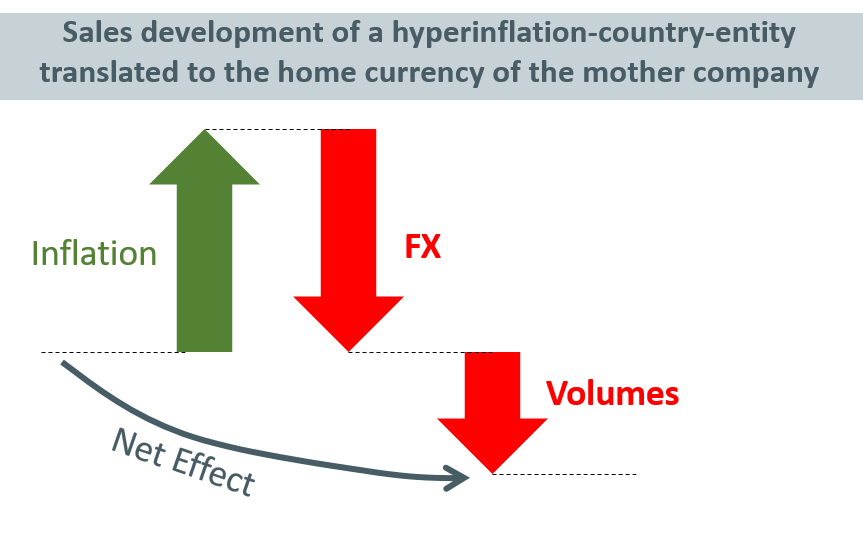

In a normal, but high-inflation environment, there are two-and-a-half effects that impact sales growth. First, of course, inflation drives up growth rates. Second, as inflation leads to a depreciation of the local currency, the exchange rate effect has a reducing impact on sales growth if retranslated to the home currency (e.g. USD or Euro) of international companies. And the remaining half-effect, often the buying power of e.g. consumers is also impacted to a certain degree which often leads to at least slightly decreasing volumes sold and hence also to a reduction of growth. As long as the whole system is still quite stable the latter effect is not super-relevant and the net economic impact on sales growth rates (as compared to a normal low inflation world) is rather low.

This, however, changes if inflation rates are getting higher and higher. Then we can often observe that the buying power erosion becomes quite massive – the half-effect becomes a full-one. While the inflation and FX effects still cancel out often (as long as there are no structural hedging policies in place which is often not reasonably possible in such market environments) but not always, the negative volume effect now fully strikes through in any way. Seen from the perspective of the home currency of most international companies this leads to a markedly net negative effect on sales development in most cases.

Important to note: In most cases that we are aware of the negative volume effect can already be found to a non-negligible extent long before inflation rate touch the territory of where either IFRS or US-GAAP qualify a country as hyperinflationary.

- How do Companies include such Effects in their organic Sales Growth Measures?

Companies disclosures do not at all provide a uniform picture. The range of disclosure strategies is quite big in reality. At least we can isolate four different core strategies.

First, Danone (and Unilever so far) excludes the entity in the hyperinflationary country at all from their overall measures. This usually has a slightly positive effect as compared to the ideal economic case.

Second, companies such as Colgate-Palmolive and Procter & Gamble include the entity’s net sales growth in local currency in the overall calculation of organic sales growth. This has a net positive growth effect as compared to the above shown economic effect (if seen in the mother’s home currency).

Third, companies like Nestlé and Unilever offer some sort of normalisation by including what they call a “normalised” price growth of 2% per month into their organic sales growth calculations. The effect is slightly positive as compared to the ideal economic case shown above (if we assume that inflation and FX more or less cancel out, i.e. purchasing power party holds).

And finally fourth: In our opinion the best (because economically sound) way is chosen by Beiersdorf AG (and partly by L’Oréal SA). The company more or less follows the economic proceeding described above, i.e. including all effects (inflation, volumes AND exchange rates) into their calculations.

- Analytical Assessment

Due to the sometimes quite remarkable quantitative effects that the choice of one of the above variants has, we want to make clear here that the first three variants do not provide a sound economic picture of the performance of companies. For an analyst, who is interested in making cash flow forecasts and determining the value of a company, the best way at our opinion is to include ALL effects into the growth rates (similar to the Beiersdorf and L’Oréal way) and additionally adapt her analytical framework for the hyperinflation case. Such analytical adaption requires in particular the following:

- Perform a macroeconomic analysis of the target country. How will the situation develop in the coming years on a country level? What does it mean for general inflation rates and exchange rate developments? This should give you an insight into general pricing levels and what this means in the home currency.

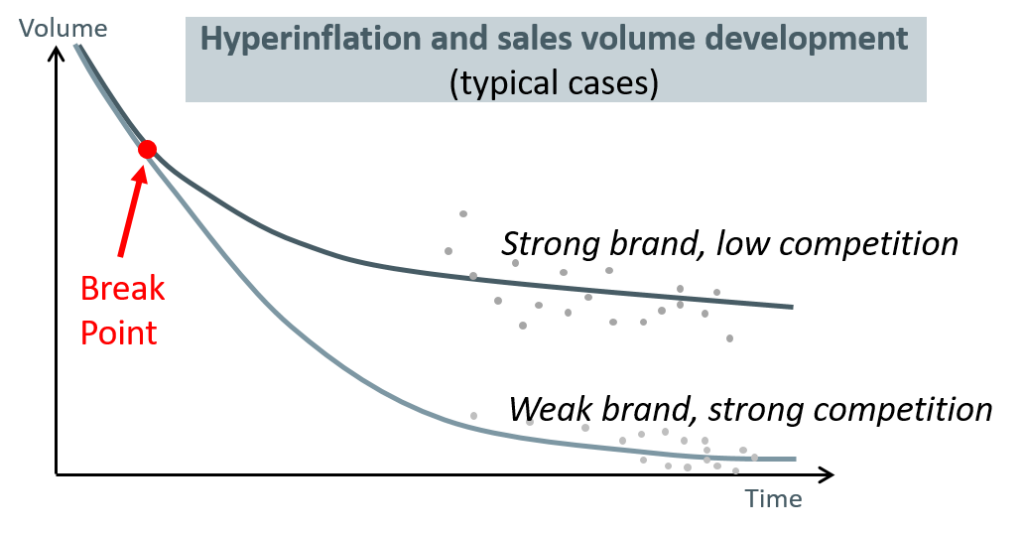

- Additionally focus on the prospective volume effect (this now becomes a company specific analysis). While we often observe that volumes go down initially quite massively for whatever product it is, the mid- to long-term path depends a lot on the quality- and marketing-moat as well as the competitive situation for the specific products. This requires a deep dive into a) the competitive situation in the respective local product markets, and b) the brand power of the products/companies. For consumer staples companies many products serve a daily requirement of consumers. There is no endless reduction in demand because at some point consumers need (or at least buy) the products anyway. Hence, hyperinflationary environments should always trigger some new fundamental analytic perspectives. And such analysis often sheds a bright light on where the real bottom of volume reductions might be.

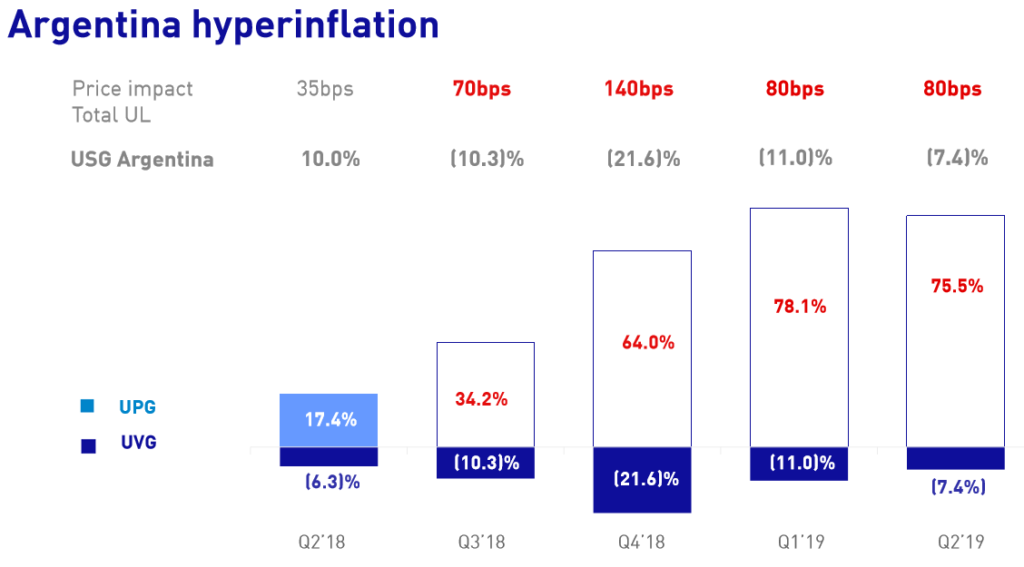

E.g., in the case of Unilever this bottoming-out effect is shown in the graph below. The recent Q2/2019 results presentation indicates that in the first two quarters of this year the volume reductions (here shown by the dark blue bar “UVG”: Unilever Volume Growth) have reduced despite still ultra-high inflation rates.

Source: Unilever Q2/2019 results presentation, p. 16.

Summary

Hyperinflationary situations are quite tricky to manage for equity investors and analysts. Accounting standard setters have different definitions of what “hyperinflationary” means, the concrete application following US-GAAP differs from that of IFRS, and companies make use of this confusion by providing e.g. a very broad range of organic growth rate definitions.

The best way to deal with this is a) to make it stand on economic feet and b) add some more analytical power and effort to the hyperinflation situation.